Introduction

Funeral insurance helps cover the costs of end-of-life expenses, such as burial, cremation, memorial services, and other final arrangements. Also known as burial insurance or final expense insurance, this type of policy provides peace of mind for both individuals and their loved ones.

But did you know that funeral insurance laws and regulations can vary depending on where you live? Every U.S. state has its own rules when it comes to insurance licensing, benefit payouts, pre-need funeral contracts, and consumer protections.

This guide breaks down the key funeral insurance rules and regulations by state, so you can make a smart and informed decision no matter where you live.

What Is Funeral Insurance?

Before we jump into the state-specific laws, let’s review what funeral insurance actually is. Funeral insurance is a small whole life insurance policy designed to pay out a lump sum—typically between $5,000 and $25,000—directly to your beneficiary or funeral home when you pass away.

This money is meant to cover expenses like:

- Funeral or cremation costs

- Burial plots and caskets

- Headstones or urns

- Memorial services

- Obituaries and death certificates

Funeral insurance is especially popular with seniors, those planning ahead for their families, and people who may not qualify for traditional life insurance due to age or health issues.

Why Laws Differ by State

Each state regulates insurance through its own Department of Insurance. That means rules about who can sell funeral insurance, how benefits are paid, and what rights consumers have can vary.

Some states are stricter in regulating pre-need funeral plans (which are paid directly to funeral homes), while others offer more flexibility. Understanding your state’s laws ensures you don’t face issues when it’s time for your loved ones to access your policy.

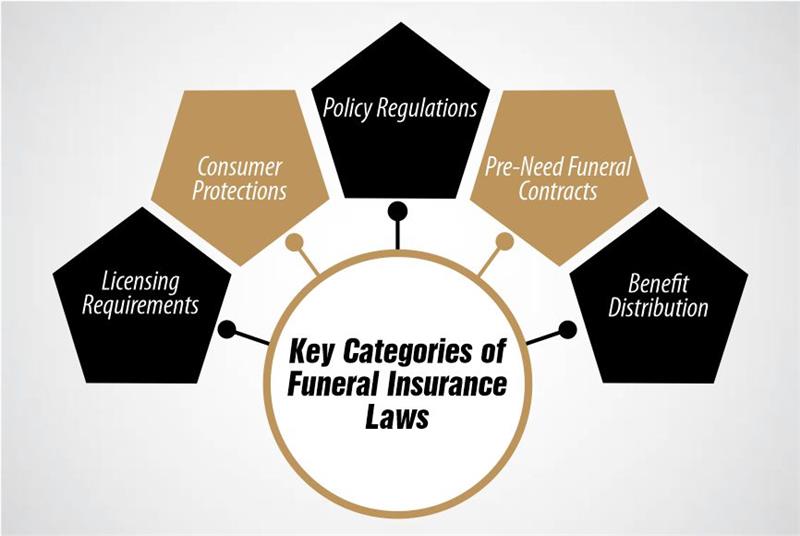

Key Categories of Funeral Insurance Laws

Across states, most funeral insurance laws fall into these categories:

- Licensing Requirements: Who is allowed to sell insurance policies?

- Consumer Protections: Are there laws protecting buyers from fraud or abuse?

- Policy Regulations: Are waiting periods, exclusions, and premium structures regulated?

- Pre-Need Funeral Contracts: Are funeral homes allowed to sell insurance-based contracts directly?

- Benefit Distribution: Can benefits go directly to a funeral provider, or must they go to a named beneficiary?

Now let’s explore how these regulations apply across different U.S. states.

Regional Breakdown of Funeral Insurance Laws

For easier reading, we’ve grouped the states by region and summarized their key rules.

Northeast States

New York

- Strictly regulates funeral prepayment plans.

- All funds must be placed in trust.

- Only licensed agents can sell insurance.

Massachusetts

- Insurance agents must be licensed by the state.

- Funeral homes cannot act as insurance agents.

Pennsylvania

- Allows pre-need insurance contracts.

- Consumers must receive detailed contract disclosures.

Midwest States

Illinois

- Regulated by the Department of Insurance and the Comptroller’s Office.

- Funds from pre-need plans must be held in a trust or insurance policy.

Ohio

- Allows both insurance-funded and trust-funded funeral plans.

- Insurance companies must follow detailed disclosure rules.

Michigan

- Licensed funeral homes may offer prepaid funeral contracts.

- Strict laws about where funds are held and how they’re used.

Southern States

Texas

- Requires insurance agents to be licensed.

- Allows pre-need insurance through funeral homes with oversight.

- Texas Department of Banking monitors trust arrangements.

Florida

- Strong consumer protection laws for pre-need plans.

- Sellers must disclose all fees and cancellation policies.

Georgia

- Requires a Pre-Need Sales Agent license.

- Insurance-backed funeral plans must meet funding requirements.

Western States

California

- Funeral insurance must be sold by a licensed insurance agent.

- All funeral homes must register with the Cemetery and Funeral Bureau.

Arizona

- Allows funeral homes to sell pre-need plans with proper licensing.

- Requires a trust or insurance policy to back prepaid arrangements.

Washington

- Detailed regulation of pre-arranged funeral plans.

- Funds must be placed in trust or backed by an insurance company.

How to Find Your State’s Rules

To find the exact laws for your state, follow these steps:

- Visit Your State’s Department of Insurance Website

Most states list licensing, consumer rights, and funeral insurance rules clearly. - Search for Pre-Need Funeral Insurance Laws

This search can lead you directly to funeral board guidelines and legal documents. - Speak to a Licensed Insurance Agent in Your State

A local agent understands state-specific rules and can guide you in choosing the right policy. - Contact the Funeral Consumer Alliance

They offer state-by-state funeral planning resources and legal advice.

Red Flags to Watch For

No matter where you live, be cautious of:

- Unlicensed Agents: Always verify licensing through your state’s insurance website.

- Lack of Transparency: Walk away from any plan that doesn’t clearly explain costs, benefits, or exclusions.

- Pressure Tactics: You should never feel rushed into buying funeral insurance.

Tips for Buying Funeral Insurance in Any State

- Compare at Least 3 Plans: Get quotes from multiple providers to compare premiums and benefits.

- Read the Fine Print: Pay special attention to waiting periods and exclusions.

- Involve a Trusted Family Member: It’s always smart to have a second set of eyes review the policy with you.

- Make Sure It’s Portable: Choose a plan that stays valid if you move to another state.

- Keep Documents Handy: Store your funeral insurance policy with your will or other estate planning documents.

Frequently Asked Questions (FAQs)

Q: Do all states allow funeral homes to sell funeral insurance?

No. Some states restrict funeral homes from directly selling insurance and require licensed agents to handle all transactions.

Q: Can funeral insurance benefits go straight to the funeral home?

Yes, in many states you can assign the benefit directly to a funeral provider. Just make sure it’s noted in the policy.

Q: What happens if I move to another state?

Most policies are portable, but always check with your provider to confirm.

Q: Are there tax implications for funeral insurance payouts?

Generally, funeral insurance benefits are tax-free, but consult a tax advisor for personalized advice.

Conclusion

Funeral insurance is a thoughtful way to plan ahead and protect your loved ones from unexpected financial stress. But the rules that govern these policies aren’t the same in every state.

By understanding how your state regulates funeral insurance—whether it’s through licensing, consumer protections, or pre-need funeral contracts—you can confidently choose the right policy for your needs.

Always work with a licensed professional, read the policy carefully, and make sure your coverage is legally sound and sufficient for your final wishes.